Sustainability in multifamily real estate is no longer just about energy-efficient systems and green certifications. It’s about something much harder: changing resident behavior. The operators making real progress on sustainability recognize that infrastructure and intention have to work together, and that lasting change starts with making the sustainable choice the easy choice.

The U.S. multifamily green building sector is currently valued at approximately $43.8 billion, and globally the green building market exceeded $530 billion in 2024, projected to grow at a 10.2% CAGR through 2034.¹ Multifamily investment firms are increasingly using ESG criteria to evaluate and guide acquisitions, a trend that has accelerated significantly heading into 2026.²

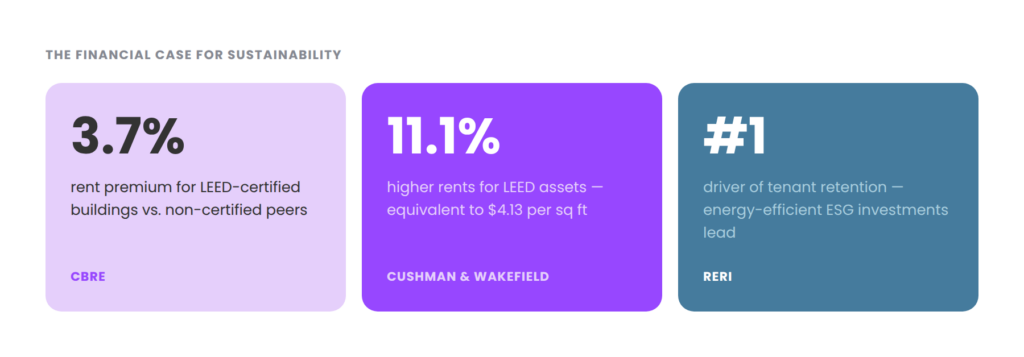

The financial case is clear: LEED-certified multifamily buildings earn a 3.7% rent premium over non-certified peers after controlling for age, size, and location, according to CBRE research.³ A Cushman & Wakefield study put that figure even higher, finding LEED-certified assets averaging 11.1% higher rents, or $4.13 per square foot, versus non-certified buildings.⁴ Research from the Real Estate Research Institute further found that cost-saving ESG investments, particularly energy efficiency, are among the most effective tools for retaining tenants in multifamily properties.⁵

And yet the demand signal from residents is outpacing operator response. According to the 2024 NMHC/Grace Hill Renter Preferences Survey (the industry’s most comprehensive study of renter sentiment, drawing on input from over 172,000 renters across 4,220 communities) nearly 60% of respondents said building and sustainability certification would positively influence their rental decision.⁶ A separate NMHC/Kingsley survey found that more than 60% of renters consider environmentally friendly factors essential when choosing where to live.⁷ Yet despite this demand, only 12% of landlords report actively prioritizing sustainability in their properties.⁸ That gap between what residents want and what operators deliver is both a problem and an opportunity.

From Compliance to Culture and the Infrastructure That Makes It Stick

The operators closing the gap between renter demand and on-the-ground reality are the ones treating sustainability as a cultural initiative, not a compliance exercise. Guillaume Deri at Greystar France offers a telling example:

“We try our best to embed people. We do events like clothing exchanges, for instance — and the vintage vibe is working well on the residents.” — Guillaume Deri, Greystar France

Clothing swaps, vintage markets, and community exchange events transform sustainability from an obligation into a social experience. When green behavior becomes part of a community’s identity, it’s far more likely to stick than when it’s mandated through signage and rules. Research backs this up: studies on shared-use programs like Library of Things found that roughly 1 in 4 users avoided a purchase entirely after accessing a shared alternative, a meaningful behavior shift that compounds over time. And that instinct runs even deeper in the generation now driving multifamily demand.

But culture alone isn’t enough. Yael Shemer, Co-Founder of TULU, identifies the deeper enabler:

“You can’t ask people to change behavior without offering infrastructure. Building an infrastructure is the first accelerating thing to do.” — Yael Shemer, Co-Founder, TULU

This is what separates aspiration from action. Residents may want to live more sustainably, but if the infrastructure doesn’t support it, if recycling is confusing, sharing is impractical, or alternatives are unavailable, good intentions stall. The operator’s role is to build the systems that make the sustainable choice the frictionless one. Culture and infrastructure aren’t competing strategies. They’re the same strategy, working at different layers.

What Impact Looks Like at Scale

The data from TULU’s own operations illustrates what happens when infrastructure is built with behavior change in mind. With 250,000+ users across 500+ buildings in over 60 cities, TULU’s model shows the compounding power of access over ownership.

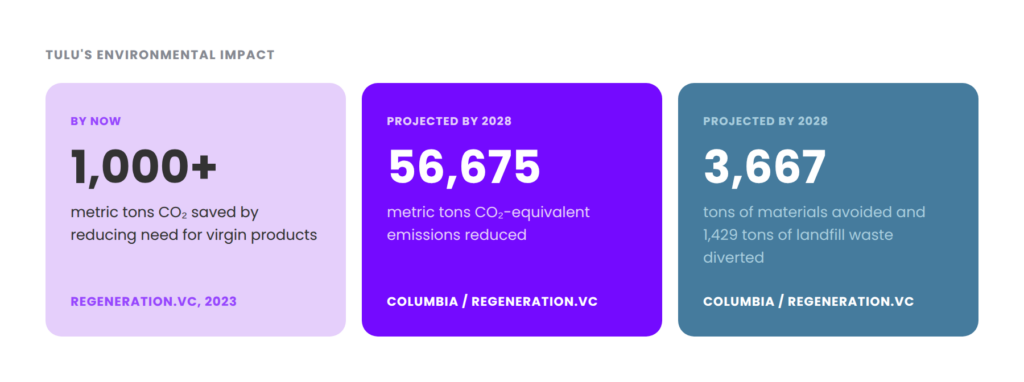

Based on analysis from Regeneration.VC and a Columbia University sustainable investing research project, TULU has already saved 1,000+ metric tons of CO₂, conserved 25 million+ liters of water, and avoided over 200,000 kg of materials, to date.⁹ By 2028, the cumulative projected impact grows significantly: an estimated 56,675 tons of CO₂-equivalent emissions reduced, 3,667 tons of materials avoided, and 1,429 tons of landfill waste diverted.¹⁰ Those figures are grounded in peer-reviewed Life Cycle Assessment data on vacuum cleaners, extrapolated to other top-rented products across TULU’s network.

These numbers have been cross-referenced against industry benchmarks and hold up: TULU’s model delivers approximately 8.75 kg of CO₂e saved per rental — consistent with the 7–12 kg per rental range reported in comparable impact assessments.¹¹

The model also directly addresses the regulatory pressures bearing down on building owners. In New York City alone, more than 50,000 buildings are now subject to Local Law 97, with emissions caps and fines in effect since 2024. Dozens of other cities, Boston, Seattle, Washington D.C., are enacting similar building decarbonization legislation, with residential buildings of 150+ units squarely in scope.¹² For operators navigating LEED, WELL, and ESG reporting requirements, shared-use infrastructure like TULU contributes measurable Scope 3 emissions reductions and tenant engagement data that supports compliance, while simultaneously contributing to the rent premium and retention outcomes the research consistently shows are tied to certified, sustainable buildings.

The Takeaway

The story of sustainable multifamily isn’t really about buildings, it’s about people, and what happens when you stop asking them to change and start building environments that make change feel natural.

Residents across the country already want to live more sustainably. They’re choosing buildings based on green certifications. They’re drawn to communities where sharing feels normal and ownership feels optional. The intention is there. What’s often missing is a building that meets them halfway: one where the recycling system makes sense, where borrowing a vacuum is easier than buying one, where a clothing swap in the lobby turns a chore into a social event.

The operators who understand this aren’t treating sustainability as a compliance checkbox or a marketing angle. They’re treating it as a design problem: how do you build a place where the right choice is also the easy one? That requires infrastructure, shared-use systems, thoughtful amenity design, data that tells you what residents actually need. And it requires culture, programming, community, the kind of belonging that makes green habits feel like identity rather than obligation.

Neither works without the other. Infrastructure without culture is just unused equipment and culture without infrastructure is just good intentions. Together, they’re how lasting behavior change actually happens: quietly, incrementally, one rental and one swap at a time.

Sources

- Green Building Market Size & Share, Statistics Report 2034 — Global Market Insights (2024)

- 2026 Multifamily Property Management Trends to Watch — Parcel Pending (December 2025)

- Value of Environmental Building Features — Strengthening Value Through ESG — CBRE

- “Green is Good” research series — Cushman & Wakefield

- “ESG and Occupant Retention in Multifamily Apartments” — Real Estate Research Institute (RERI)

- 2024 NMHC/Grace Hill Renter Preferences Survey Report — NMHC & Grace Hill (November 2023) — based on 172,703 renters in 4,220 communities

- What Renters Want in 2025 — SmartRent, citing NMHC/Kingsley Associates Renter Preferences Survey (May 2025)

- “2024 Trends in Multifamily: Retention is Key” — ICT, Integrated Control Technology (May 2024)

- TULU Environmental Impact Report — based on Regeneration.VC 2023 Impact Analysis

- TULU Impact Calculator — Columbia University / Regeneration.VC, 2024 Sustainable Investing Research Consulting Project (2028 projections)

- TULU Impact Cross-Reference Table — benchmarks sourced from WRAP UK circularity data, SimaPro/Ecoinvent LCA datasets, EU Product Environmental Footprint Methodology

- Local Law 97 — Building Emissions — NYC.gov